Tax-loss harvesting sounds technical. The core idea is simple.

When a position is down, you can sell it, realize the loss for tax purposes, and buy a similar replacement so your portfolio stays invested. The market exposure stays roughly intact. The tax bill gets better.

That is the whole game. Everything else is execution quality: lot tracking, wash-sale avoidance, replacement selection, and timing.

The basic mechanic

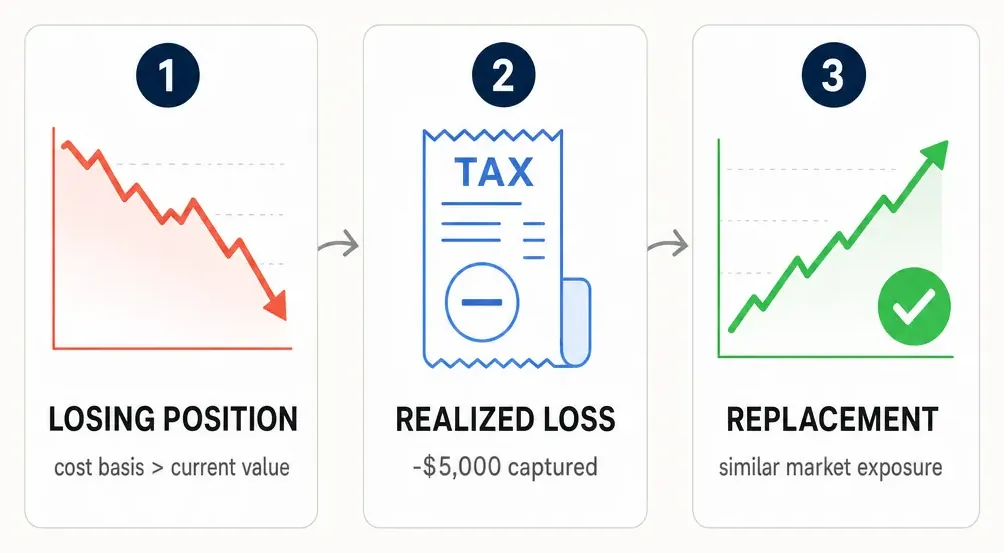

Say you bought an S&P 500 ETF at $400 and it is now worth $360. You are down $40 per share. If you simply hold it, that loss is still just paper. The IRS does not care about unrealized losses.

If you sell, the loss becomes real. Then you can buy a replacement with similar exposure so your portfolio is not sitting in cash. In practice, a tax-aware workflow looks like this:

- Sell the losing position.

- Realize the capital loss.

- Buy a replacement that preserves your market exposure without tripping the wash-sale rule.

The result is what matters: you are still invested, but now you own a documented loss that can offset gains.

What the loss is worth

Losses offset capital gains dollar for dollar. If losses exceed gains, up to $3,000 per year can offset ordinary income, and the rest carries forward.

That means the value of a harvested loss depends on your tax situation. For a high-income investor in a high-tax state, a $10,000 harvested loss can be very meaningful. For someone in a zero-percent capital-gains year, it may be much less valuable right now.

This is why serious TLH should be thought of as a tax-alpha engine, not a generic trading trick.

The wash-sale rule is the line between smart and sloppy

The IRS blocks the obvious abuse: you cannot sell at a loss and immediately buy back the same or substantially identical security just to manufacture a deduction.

That is the wash-sale rule. And it is the reason naive TLH software fails in the real world.

A good TLH workflow does not just say, "Sell the loser." It asks:

- What other accounts in the household hold this exposure?

- What replacement keeps the portfolio aligned?

- What purchases happened in the 30-day window before the sale?

- Will this create a hidden problem in a spouse account or IRA?

If you want the full rule set, read The wash-sale rule, demystified.

Why direct indexing changes the economics

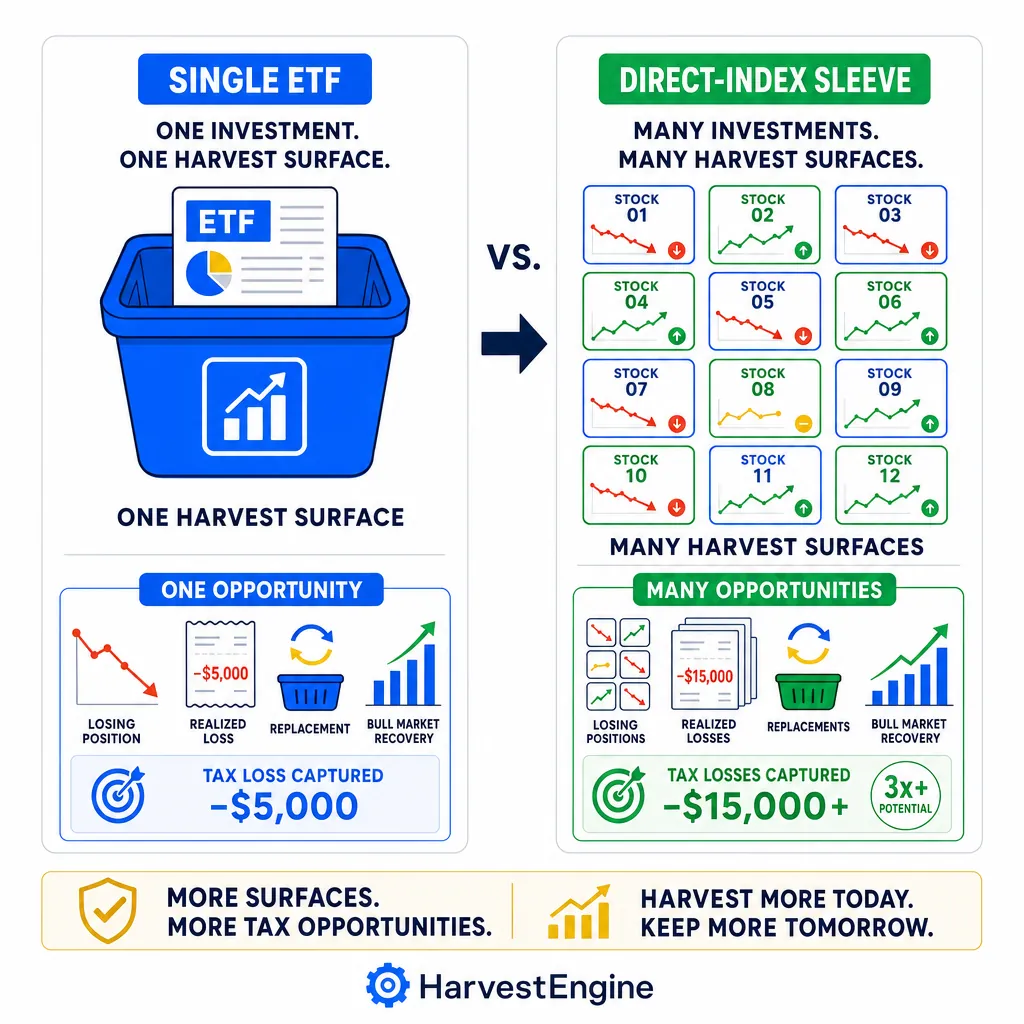

One ETF gives you one position. A direct-index sleeve gives you dozens of positions. That changes the harvest surface completely.

When you hold a single ETF, you only have a harvest opportunity when the ETF itself is down. When you hold a basket of stocks, many individual names can be down even when the index is flat or up.

That is the core reason direct indexing matters. It turns one harvest surface into many. It is not about beating the market. It is about creating more tax-lot opportunities while staying tied to the same benchmark exposure.

That is also why direct indexing is not for everyone. The account size, tax bracket, and time horizon all matter.

What good TLH software actually has to do

Most explanations stop at "sell the loser, buy a replacement." That is enough for a cocktail-party summary, not a real product.

A real TLH engine has to:

- track every tax lot, not just the total position

- rank opportunities by tax value, not just percentage loss

- avoid wash sales across the household

- choose replacements that preserve sector, beta, and benchmark fit

- check that the tax value is worth more than the transaction friction

- keep the whole portfolio inside a tracking-error budget

That is the difference between a screenshot feature and a portfolio system.

The long-term payoff

Harvested losses do not just help this year. They build a loss bank you can use later when you rebalance, diversify a concentrated position, or realize gains in a year where you actually want the liquidity.

That is why TLH gets more powerful when it is treated as a process, not an occasional event. The compounding benefit is not just market return. It is optionality.

How HarvestEngine thinks about it

HarvestEngine is built around a simple idea: TLH should feel like a serious portfolio workflow, not a gimmick.

- Connect your existing brokerage.

- Build a direct-index sleeve that maps to your benchmark.

- Scan for loss opportunities continuously.

- Score the replacements and the exposure tradeoffs.

- Show the proposed trades clearly before anything happens.

That is the architecture I wanted for myself, and it is why HarvestEngine exists.

From here, the cleanest next reads are Direct indexing in 2026, TLH vs ETF rebalancing, Why the algorithm matters (the actual logic the engine runs on every position), and Why subscriptions beat percentage-of-assets fees.