Concentrated stock is one of the hardest portfolio problems because the risk and the tax cost fight each other.

If you sell too much too fast, the tax bill can be painful. If you sell too slowly, one ticker keeps dominating the household balance sheet. If you do nothing, you are still making a decision, just not a very controlled one.

The real question

What is the right question to ask when managing a concentrated stock or RSU position?

The right question is not simply whether to diversify — in many cases the direction is obvious — but how to reduce concentration with the lowest total cost, weighing capital-gains taxes from selling, ongoing concentration risk from holding, and the opportunity cost of delay.

The right question is not simply "should I diversify?" In many cases, diversification is the obvious direction.

The better question is: how do I reduce concentration with the lowest total cost?

Total cost includes:

- capital-gains tax from selling

- ongoing concentration risk from holding

- the opportunity cost of delaying a better portfolio structure

Why this problem is different

Why is concentrated stock harder to manage than a normal rebalancing decision?

Concentrated stock is usually the byproduct of success or long tenure — it is emotionally sticky, the tax consequences of fixing it in one shot can be severe, and the right answer is rarely a single dramatic sale but rather a structured path that balances tax cost against risk reduction over time.

Concentrated stock is not a normal rebalance problem. It is usually the byproduct of success, long tenure, or both. That makes it emotionally sticky. The investor knows the risk is real, but also knows the tax consequences of fixing it in one shot can be severe.

That tension is exactly why a more structured process helps.

The tools that actually matter

What are the most effective tools for reducing concentrated stock exposure while managing the tax cost?

Building a loss bank in other accounts, pacing the unwind over multiple years, and reinvesting with intent into a direct-index sleeve designed around remaining exposure are the three levers that can reduce concentration while limiting the immediate tax hit.

1. Build a loss bank elsewhere

If the investor has other taxable assets, tax-loss harvesting in those accounts can build a reserve of realized losses that may later help offset gains recognized from diversification.

This is one of the least obvious benefits of disciplined TLH. The value is not just current-year savings. It is future flexibility.

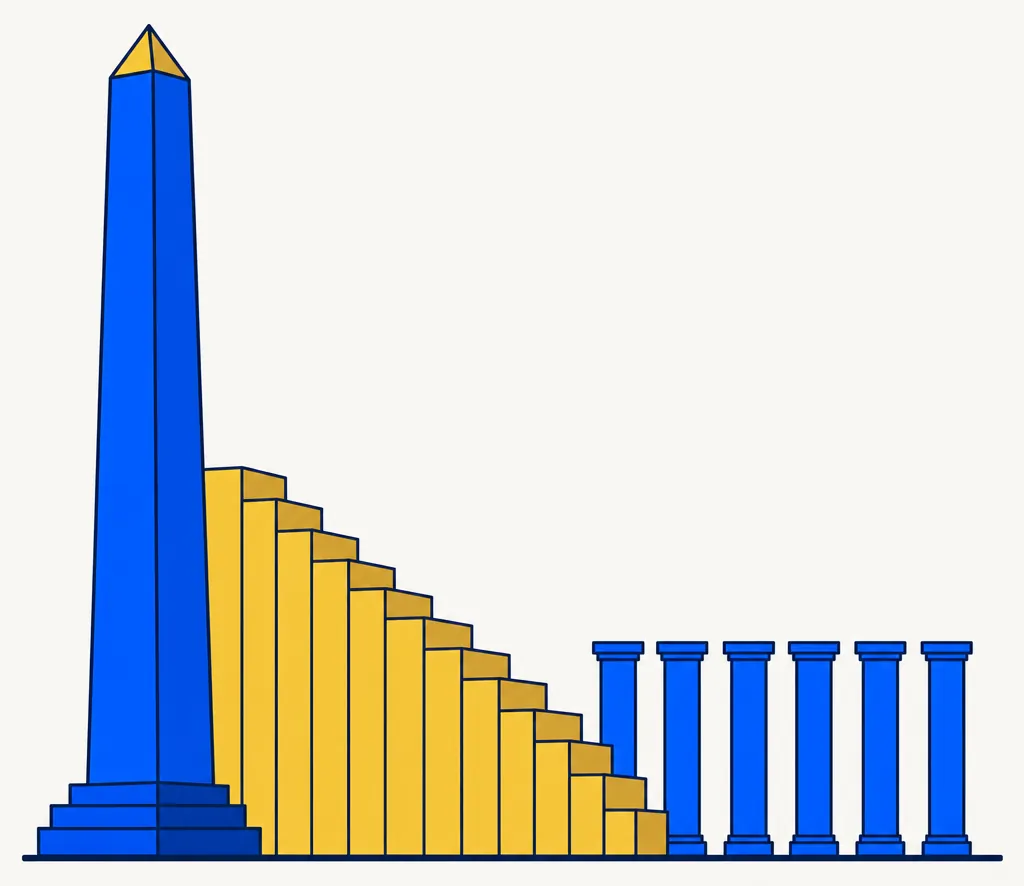

2. Pace the unwind

Many concentrated positions are better handled through a staged reduction instead of one dramatic sale. The right pace depends on tax profile, risk tolerance, and how concentrated the position actually is.

3. Reinvest with intent

Replacing concentrated stock with a generic ETF can still leave a lot of sector overlap. A direct-index sleeve or completion portfolio can be a more thoughtful reinvestment target because it can be designed around the exposure that remains.

Why direct indexing is useful here

Why is a direct-index sleeve a stronger reinvestment choice than a generic ETF when diversifying out of concentrated stock?

A direct-index sleeve can be designed to reduce overlap with the concentrated name, improve diversification at the household level, and create tax-lot flexibility going forward — a much stronger answer than a one-size-fits-all ETF reinvestment.

Direct indexing gives the investor more control over the shape of the replacement portfolio.

Instead of simply saying "sell and buy the market," a direct-index sleeve can be designed to:

- reduce overlap with the concentrated name

- improve diversification at the household level

- create tax-lot flexibility going forward

That is a much stronger answer for a concentrated-stock holder than a one-size-fits-all reinvestment suggestion.

What HarvestEngine can help make visible

What should a tax-aware product show an investor managing a concentrated stock unwind?

A serious product should surface how concentrated the household actually is, what unwind pace is being considered, how much realized loss capacity exists elsewhere, and what the replacement sleeve looks like after each sale — the information that makes the tradeoff legible.

A good product should help the user see:

- how concentrated the household really is

- what unwind pace is being considered

- how much realized loss capacity exists elsewhere

- what the replacement sleeve looks like after each sale

That is where software can add real value. Not by pretending there is one perfect answer, but by helping the user work through a complicated planning problem with more clarity.

The big takeaway

What is the core insight for investors managing a concentrated stock or RSU position over time?

Concentrated stock is not just a decision about whether to sell — it is a multi-year path from an overconcentrated starting point to a more durable portfolio, where tax-awareness throughout the unwind can materially change the total cost of getting there.

Concentrated stock is not just about deciding whether to sell. It is about designing a path from an overconcentrated starting point to a more durable portfolio while staying aware of taxes the entire way.

That is why this topic belongs next to the zero-tax exit strategy, tax alpha explained, and the art of pacing. They are all parts of the same conversation.